A Crisis Europe Thought It Had Outgrown

By ICTpost Global Energy & Geopolitics Bureau

Europe thought it had closed the chapter on energy shock.

After Russia’s invasion of Ukraine in 2022 ripped through gas markets and pushed inflation to record highs, governments across the continent scrambled to adapt. Russian pipeline gas was replaced with liquefied natural gas (LNG), strategic storage rules were tightened, renewables were fast‑tracked and emergency measures institutionalised.

By late 2024, policymakers believed the system had stabilised.

That confidence is now being tested again.

The escalation of conflict involving Iran has pushed energy back to the centre of Europe’s economic vulnerability, reigniting fears of inflation, disrupted growth and renewed pressure on the euro. The trigger is familiar: geopolitics colliding with energy supply. This time, the fault line runs through the Middle East.

The Strait That Moves the Market

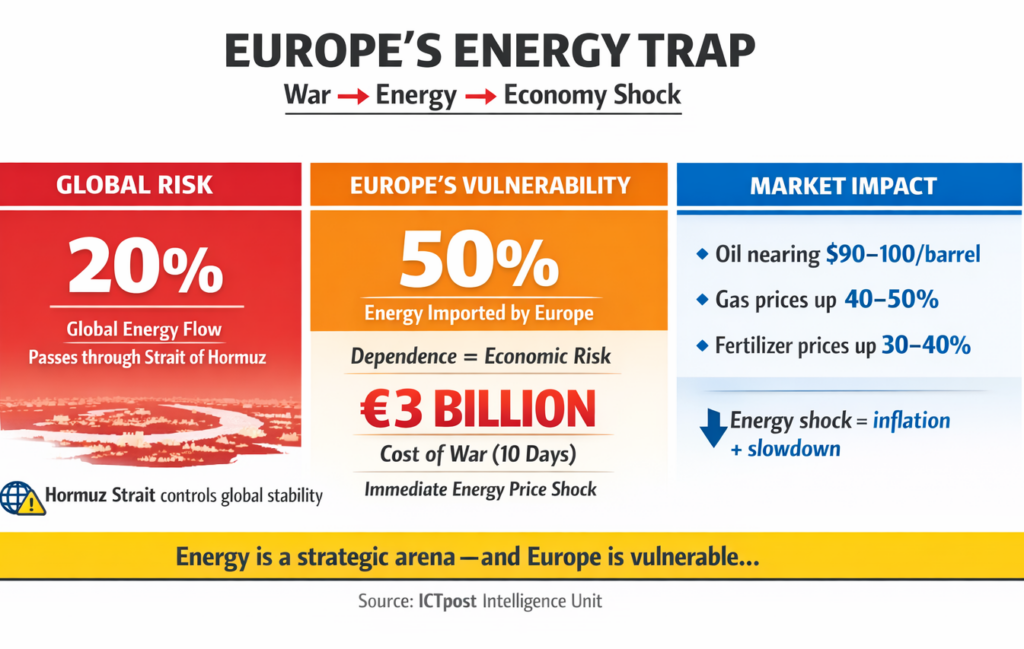

At the heart of the shock lies the Strait of Hormuz, a narrow maritime corridor through which roughly one‑fifth of global oil and liquefied natural gas normally flows, according to the U.S. Energy Information Administration.

Since hostilities escalated, tanker traffic through the strait has fallen sharply. Insurers have withdrawn cover, shipowners are avoiding the route and producers across the Gulf have been forced to slow output as storage fills up.

Reuters mapping of the disruption warns it represents one of the most serious energy shocks since the Ukraine war, with spare capacity elsewhere unable to compensate quickly.

https://www.bloomberg.com/news/articles/2026-03-10/how-the-iran-war-is-disrupting-global-oil-and-gas-supply tanker traffic through the strait has dropped close to a halt, forcing producers such as Saudi Arabia to cut output as storage fills.

Markets reacted immediately. Brent crude surged back toward the $90–$100 a barrel range. European gas benchmarks posted some of their largest weekly jumps in years, and LNG availability tightened as shipping delays mounted. Asian buyers began bidding aggressively for cargoes, diverting supply away from Europe just as it began refilling storage after winter.

As International Energy Agency chief Fatih Birol warned, “We are witnessing the first truly global energy crisis.”

Europe’s Exposure — Quantified, Not Asserted

Europe’s vulnerability is not abstract; it is measurable.

According to Eurostat’s Energy in Europe 2026 release, the EU imported 57% of its total energy needs in 2024, leaving the bloc structurally exposed to global price shocks rather than shielded by domestic supply (Eurostat).

Oil and petroleum products accounted for 67% of imports, while natural gas made up another 24%.

The underlying driver is not rising demand but declining domestic production. A Federal Reserve analysis shows that while renewables have expanded rapidly, they have failed to offset falling hydrocarbons and nuclear output, keeping Europe dependent on imports for marginal supply (Federal Reserve).

Why Hormuz Is a Bigger LNG Shock Than Ukraine

The 2022 crisis was fundamentally a pipeline shock. Europe replaced Russian gas with LNG.

This crisis strikes the LNG system itself.

Roughly 20% of global LNG trade transits the Strait of Hormuz, primarily from Qatar. LNG cargoes move to whoever pays the highest price, and when supply tightens, Asia usually outbids Europe.

Reuters flow data shows that around 83% of LNG passing through Hormuz normally goes to Asia, not Europe, meaning European access depends on price competition rather than security of supply (Reuters).

CNBC, citing Rapidan Energy, warns LNG disruption could ultimately prove more damaging than oil, due to restart complexity and persistent shipping insurance constraints (CNBC).

Gas Storage Is a Buffer — Not a Solution

Gas storage buys time but does not replace supply.

The European Commission acknowledges storage provides 25–30% of winter gas demand, while warning that rigid filling rules can amplify price pressure during global shocks (https://ec.europa.eu/commission/presscorner/detail/en/qanda_25_668).

New modelling from Gas Infrastructure Europe shows that under stress conditions, deliverability — not volume alone — becomes the binding constraint, with storage supplying over half of peak winter demand in prolonged disruptions (GIE).

German storage operators further warn that global LNG competition has flipped the summer‑winter spread negative, removing commercial incentives to refill storage (INES).

Inflation Re‑enters Through the Energy Channel

Energy shocks do not rise in isolation.

ECB‑linked and Bank of Italy research shows energy accounted for up to 60% of peak euro‑area inflation during the 2022 crisis (SUERF / Bank of Italy).

ECB modelling confirms fuel price pass‑through is rapid and near‑complete, while gas and electricity price effects are slower but persistent — a dangerous mix if shocks endure (ECB).

European gas prices jumped sharply again in early March, reviving fears of renewed inflation momentum.

Germany’s Confidence Shock

The impact is already visible in Germany.

In March, the ZEW investor expectations index collapsed from optimism into negative territory — one of its sharpest drops since the Ukraine invasion. Investors cited higher energy prices, inflation risks and fears of a stalled recovery.

Energy‑intensive sectors such as chemicals, steel and manufacturing remain especially exposed.

https://www.euronews.com/business/2026/03/18/german-investor-confidence-collapses-on-middle-east-tensions the shift as a warning sign for Europe’s broader recovery.

Pressure Builds on the Euro

Currency markets rarely wait for confirmation.

Rising energy import bills widen trade deficits and raise dollar demand to pay for fuel, steadily pressuring the euro. Uncertainty over growth, inflation and policy coordination pushes capital toward more energy‑secure economies.

https://www.reuters.com/markets/currencies/energy-prices-eurozone-risks-2026-03-15/ warns prolonged high energy prices could keep the euro under sustained pressure.

As European Commission President Ursula von der Leyen has emphasised, “Energy security is a question of sovereignty.”

Climate Ambition Meets Economic Reality

The renewed shock is reopening difficult policy debates.

While Europe remains committed to aggressive decarbonisation, soaring prices are reviving calls to soften carbon costs, intervene in emissions markets or shield industry from green levies.

Bruegel warns that although Europe reduced reliance on Russian energy, it remains exposed to global fossil‑fuel volatility and geopolitical risk (https://www.bruegel.org/policy-brief/dependence-fossil-fuels-remains-europes-biggest-worry).

A Political Test as Much as an Economic One

Energy crises rarely remain economic for long.

Disagreements are resurfacing across the EU over burden‑sharing, coordination and emergency intervention. As in past crises, unity becomes harder precisely when it matters most.

IMF Managing Director Kristalina Georgieva cautions that “geopolitical fragmentation is increasingly shaping the global economic outlook.”

A Familiar Question, Revisited

Much now hinges on how long the conflict lasts.

A rapid de‑escalation could limit damage. A prolonged disruption risks locking Europe into persistently high energy costs, weaker growth and renewed pressure on the euro.

But the deeper issue is not this war.

It exposes an energy system that has been stabilised — but not transformed. Europe remains exposed to shocks beyond its control, politically strained under pressure and economically sensitive to conflicts far from its borders.

In today’s world, energy security is economic sovereignty.

Once again, that sovereignty is under strain.

editor@ictpost.com